How To Repair A Broken Iron Condor

Home : Options Strategies

Long Iron Condor and Short Atomic number 26 Condor

In this chapter, we shall hash out ii option strategies: Long Iron Condor and Brusk Fe Condor. We shall talk almost the various aspects of these two strategies including payoffs, Greeks, and illustrations with examples.

LONG Iron CONDOR

| Strategy Details | |

| Strategy Type | Neutral on management, merely bullish on volatility |

| # of legs | iv (Short 1 Lower Strike Put + Long 1 Lower Middle Strike Put + Long 1 Higher Middle Strike Telephone call + Brusk 1 Higher Strike Call) |

| Maximum Reward | Lower Heart Strike Price - Lower Strike Cost - Net Premium Paid |

| Maximum Risk | Express to the extent of internet premium paid |

| Lower Breakeven Price | Lower Eye Strike Cost - Net Premium Paid |

| Upper Breakeven Price | Higher Middle Strike Price + Net Premium Paid |

| Payoff Calculation | Payoff of lower strike Short Put+ Payoff of lower centre strike Long Put + Payoff of college eye strike Long Call + Payoff of higher strike Short Call |

Explanation of the Strategy

A Long Iron Condor is a strategy wherein the trader would sell a lower strike Put, buy a lower center strike Put, buy a higher middle strike Call, and sell a higher strike Call. Each of the selection that is traded under this strategy must vest to the aforementioned underlying and must accept the aforementioned expiration. Usually, the lower strike and the lower centre strike Puts are OTM Puts, whereas the college heart strike and the higher strike Calls are OTM Calls. At the time of initiating this strategy, the underlying toll is usually somewhere between the two eye strikes. Usually, all the four options are equidistant from each other. Nevertheless, this is non a hard and fast rule. Sometimes, traders keep a wider distance between the two middle strikes as compared to that betwixt the outer and the middle strike. Doing so increases the profit potential, simply besides widens the loss-making zone.

In terms of direction, a Long Iron Condor is a neutral strategy. This is because this strategy can profit either from a down move in the price of the underlying or from an upwards move. That said, this strategy is bullish on volatility and benefits during times when volatility is rising, and vice versa. This is because the college the volatility, the higher would be the probability of the position condign assisting. A Long Iron Condor has two breakeven points: lower and upper. The position is unprofitable as long equally the underlying price is within the two breakeven points and is assisting when the underlying price is outside i of the two breakeven points. Both profits and losses under this strategy are limited. Maximum profit occurs when the underlying price falls below the lower strike or rises higher up the higher strike, while maximum loss occurs when the underlying price gets stuck within the 2 middle strikes.

A Long Atomic number 26 Condor is a net debit strategy. Maximum potential profit under this strategy is usually smaller than the maximum potential loss. As a result, this strategy must preferably exist initiated by experienced option traders only. Before initiating this strategy, 1 must ever take into consideration the risk to reward ratio and must initiate merely if this ratio is adequate and worth trading for. Also, every bit we shall later run across, Long Iron Condor has a like payoff structure as a Short Call Condor or a Short Put Condor. However, at that place are differences. The major difference is that brusque Call/Put Condor strategies are cyberspace credit strategies, whereas Long Iron Condor is a net debit strategy.

Benefits of the Strategy

-

This strategy is direction neutral as the trader tin can profit from either direction, upwards or downward

-

Maximum loss under this strategy is express

-

Rise volatility has a beneficial impact on the strategy payoff

Drawbacks of the Strategy

-

The cost/risk of this strategy tends to exceed the potential reward

-

At that place are chances that the trader could lose 100% of his net investment

-

When the underlying cost is within the confines of the two middle strikes, a decline in volatility would hurt the position

-

A abrupt move below the lower strike or above the higher strike would pb to an opportunity loss every bit maximum profit potential under this strategy is capped

-

Fourth dimension decay would hurt the trader, especially when the position is unprofitable

Strategy Suggestions

-

See that you have a neutral view on the price management, but you wait volatility to increment sharply once you have initiated the position

-

Ensure that the strikes are evenly placed. In other words, come across that the distance betwixt the lower and the lower heart strike is equal to that betwixt the college middle and the higher strike

-

Withal, sometimes, traders keep the distance betwixt the ii middle strikes slightly wider than between the outer and the middle strike to account for a higher profit

-

The spread between the strikes volition exist a trade-off betwixt the cost/risk of the strategy and the potential advantage

-

The wider the difference between the adjacent strikes, the higher will exist the cost and the risk but so would be the reward, and vice versa

-

Similarly, the wider the difference between the next strikes, the wider would be the loss-making zone, and vice versa

-

As this is a neutral strategy that benefits from rising volatility, ensure that yous execute this strategy when expiration is far off, as this would requite you lot sufficient time to go right

-

As the risk/cost tends to be higher than the reward, execute this strategy only when the gamble reward ratio is adequate to you

-

Ensure there is sufficient liquidity in the underlying that is being chosen to initiate this strategy

Choice Greeks for Long Atomic number 26 Condor

| Greek | Notes |

| Delta | Delta is at or near zero at initiation. It tends to bottom out below null when the underlying price is beneath the lower strike and tiptop out above zero when the underlying price is in a higher place the higher strike. That said, while Delta does go not-zilch as the underlying price moves, it does not deviate much from zero. Equally such, changes in the price of the underlying do not have much affect on this strategy because of the fashion it is structured. |

| Gamma | Gamma is positive and is at its highest point in between the 2 eye strikes. As the underlying toll moves abroad from the midpoint of the two middle strike and approaches either the lower or the college strike, Gamma tends to motion into negative earlier bottoming out around these extreme strikes. |

| Vega | Vega is positive and is at its highest point between the 2 middle strikes, pregnant the positive impact of a rise in volatility is the greatestaround the middle strikes. Volatility benefits as long every bit the position in unprofitable. That said, Vega turns negative when the position becomes assisting, meaning rise volatility now starts hurting the position. |

| Theta | Theta is negative and is at its lowest point betwixt the two eye strikes, pregnant time decay hurts the most effectually the middle strikes. Time decay hurts the position as long equally it is unprofitable. That said, Theta turns positive when the position becomes assisting, meaning time decay now starts benefiting the position. |

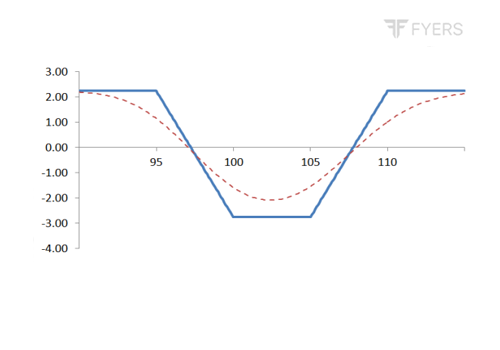

Payoff of Long Iron Condor

.PNG)

The above is the payoff chart of a Long Iron Condor. Notice that this strategy has an contrary payoff structure as compared to a Long Call Condor or a Long Put Condor. As we can meet, maximum loss under this strategy occurs when the underlying price gets stuck inside the range of the two middle strikes. On the other hand, maximum proceeds nether this strategy occurs when the underlying price either falls below the lower strike cost or rises above the college strike price. Observe that both maximum loss and gain are known beforehand and are express. Meanwhile, likewise discover that the strategy is unprofitable when the underlying price is inside the range of the two breakeven points and is profitable when the underlying price moves outside either of the two breakeven points.

Case of Long Atomic number 26 Condor

Let u.s.a. say that Mr. ABC has decided to execute a Long Fe Condor strategy on Nifty. The details of the strategy are as below:

-

Strike toll of OTM short Put = 8800

-

Strike price of OTM long Put = 9000

-

Strike cost of OTM long Call = 9200

-

Strike price of OTM short Telephone call = 9400

-

ShortPut premium (lower strike) = ₹50

-

Long Put premium (lower center strike) = ₹105

-

Long Telephone call premium (college eye strike) = ₹seventy

-

Brusque Call premium (higher strike) = ₹20

-

Net Debit = ₹105 (105 + 70 - 50 - 20)

-

Net Debit (in value terms) = ₹7,875 (105 * 75)

-

Lower Breakeven bespeak = 8895 (9000 - 105)

-

Upper Breakeven point = 9305 (9200 + 105)

-

Maximum reward = ₹vii,125 ((9000 - 8800 - 105) * 75)

-

Maximum risk = ₹7,875

At present, let usa assume a few scenarios in terms of where Nifty would be on the expiration date and the touch on this would have on the profitability of the trade.

| Underlying price at Expiration | Net Profit/Loss | Notes |

| 7000 | Profit of ₹vii,125 | Payoff = [50-Maximum of (8800-7000,0)]+[Maximum of (9000-7000,0)-105] + [Maximum of (7000-9200,0)-seventy] + [20-Maximum of (7000-9400,0)]. Equally the underlying price at expiration is beneath the lower breakeven point, the trader will brand a turn a profit |

| 8000 | Profit of ₹7,125 | Payoff = [50-Maximum of (8800-8000,0)]+[Maximum of (9000-8000,0)-105] + [Maximum of (8000-9200,0)-70] + [xx-Maximum of (8000-9400,0)]. Equally the underlying price at expiration is below the lower breakeven point, the trader volition make a profit |

| 8800 | Profit of ₹7,125 | Payoff = [50-Maximum of (8800-8800,0)]+[Maximum of (9000-8800,0)-105] + [Maximum of (8800-9200,0)-lxx] + [20-Maximum of (8800-9400,0)]. Equally the underlying price at expiration is below the lower breakeven bespeak, the trader will make a profit |

| 8850 | Profit of ₹3,375 | Payoff = [50-Maximum of (8800-8850,0)]+[Maximum of (9000-8850,0)-105] + [Maximum of (8850-9200,0)-70] + [20-Maximum of (8850-9400,0)]. Equally the underlying price at expiration is below the lower breakeven indicate, the trader will make a profit |

| 8895 | No turn a profit, No loss | Payoff = [50-Maximum of (8800-8895,0)]+[Maximum of (9000-8895,0)-105] + [Maximum of (8895-9200,0)-seventy] + [20-Maximum of (8895-9400,0)]. As the underlying toll at expiration is equal to the lower breakeven bespeak, the trader volition neither make a profit nor incur a loss |

| 8950 | Loss of ₹4,125 | Payoff = [50-Maximum of (8800-8950,0)]+[Maximum of (9000-8950,0)-105] + [Maximum of (8950-9200,0)-seventy] + [20-Maximum of (8950-9400,0)]. As the underlying price at expiration is between the two breakeven points, the trader will incur a loss |

| 9000 | Loss of ₹seven,875 | Payoff = [50-Maximum of (8800-9000,0)]+[Maximum of (9000-9000,0)-105] + [Maximum of (9000-9200,0)-70] + [xx-Maximum of (9000-9400,0)]. Every bit the underlying price at expiration is between the 2 breakeven points, the trader volition incur a loss |

| 9100 | Loss of ₹7,875 | Payoff = [50-Maximum of (8800-9100,0)]+[Maximum of (9000-9100,0)-105] + [Maximum of (9100-9200,0)-70] + [xx-Maximum of (9100-9400,0)]. Equally the underlying cost at expiration is between the ii breakeven points, the trader will incur a loss |

| 9200 | Loss of ₹7,875 | Payoff = [l-Maximum of (8800-9200,0)]+[Maximum of (9000-9200,0)-105] + [Maximum of (9200-9200,0)-seventy] + [20-Maximum of (9200-9400,0)]. As the underlying cost at expiration is between the two breakeven points, the trader will incur a loss |

| 9300 | Loss of ₹375 | Payoff = [50-Maximum of (8800-9300,0)]+[Maximum of (9000-9300,0)-105] + [Maximum of (9300-9200,0)-70] + [20-Maximum of (9300-9400,0)]. As the underlying price at expiration is betwixt the 2 breakeven points, the trader will incur a loss |

| 9305 | No profit, No loss | Payoff = [l-Maximum of (8800-9305,0)]+[Maximum of (9000-9305,0)-105] + [Maximum of (9305-9200,0)-70] + [20-Maximum of (9305-9400,0)]. Equally the underlying cost at expiration is equal to the upper breakeven signal, the trader volition neither brand a profit nor incur a loss |

| 9350 | Profit of ₹3,375 | Payoff = [fifty-Maximum of (8800-9350,0)]+[Maximum of (9000-9350,0)-105] + [Maximum of (9350-9200,0)-70] + [20-Maximum of (9350-9400,0)]. As the underlying cost at expiration is above the upper breakeven indicate, the trader will brand a profit |

| 9400 | Profit of ₹7,125 | Payoff = [50-Maximum of (8800-9400,0)]+[Maximum of (9000-9400,0)-105] + [Maximum of (9400-9200,0)-seventy] + [20-Maximum of (9400-9400,0)]. As the underlying toll at expiration is in a higher place the upper breakeven bespeak, the trader will make a turn a profit |

| 10000 | Profit of ₹7,125 | Payoff = [fifty-Maximum of (8800-10000,0)]+[Maximum of (9000-10000,0)-105] + [Maximum of (10000-9200,0)-70] + [20-Maximum of (10000-9400,0)]. Equally the underlying price at expiration is to a higher place the upper breakeven indicate, the trader will make a profit |

| 12000 | Profit of ₹7,125 | Payoff = [50-Maximum of (8800-12000,0)]+[Maximum of (9000-12000,0)-105] + [Maximum of (12000-9200,0)-70] + [twenty-Maximum of (12000-9400,0)]. Equally the underlying price at expiration is above the upper breakeven point, the trader volition make a profit |

Notice that maximum profit of ₹seven,125 for this strategy occurs when Neat either falls below the lower strike of 8800 or rises higher up the college strike of 9400. On the other hand, observe that maximum loss of ₹vii,875 occurs when Nifty gets stuck between the two middle strikes i.e. 9000 and 9200. Meanwhile, observe that the maximum risk of the strategy is greater than the maximum reward. As a event, this strategy must preferably be executed by experienced option traders merely.

Brusk IRON CONDOR

| Strategy Details | |

| Strategy Type | Neutral on direction andbearish on volatility |

| # of legs | 4 (Long i Lower Strike Put + Curt one Lower Heart Strike Put + Curt 1 College Heart Strike Phone call + Long 1 College Strike Phone call) |

| Maximum Advantage | Express to the extent of net premium received |

| Maximum Hazard | Lower Center Strike Price - Lower Strike Price - Cyberspace Premium Received |

| Lower Breakeven Price | Lower Middle Strike Price - Internet Premium Received |

| Upper Breakeven Price | College Center Strike Price + Cyberspace Premium Received |

| Payoff Calculation | Payoff of lower strike Long Put+ Payoff of lower middle strike Brusque Put + Payoff of higher middle strike Brusque Call + Payoff of higher strike Long Call |

Explanation of the Strategy

A Short Iron Condor is a strategy that involves buying a lower strike Put, selling a lower eye strike Put, selling a college center strike Telephone call, and ownership a higher strike Telephone call. Each of these options would have the same underlying instrument and expiration date. Unremarkably, the lower strike and the lower middle strike Puts are OTM Puts, whereas the higher center strike and the college strike Calls are OTM Calls. At the time of initiating this strategy, the underlying price is usually somewhere betwixt the two middle strikes. Normally, all the iv options are equidistant from each other. That said, this is not a hard and fast rule. Sometimes, to account for a wider maximum profit zone, traders prefer keeping a wider distance betwixt the two centre strikes as compared to the altitude between the outer strike and the corresponding middle strike.

A Short Fe Condor is a neutral strategy in terms of direction that works best when the underlying price consolidates. The trader who initiates this strategy would want the underlying price to stay between the two centre strikes until expiration. Hence, information technology can be said that this strategy is neutral on direction and bearish on volatility. That said, sometimes this strategy tin can take a slight bullish or surly tilt. For case, at the time of initiation, if the underlying price is beneath the 2 middle strikes, the strategy would be slightly bullish. On the other hand, if the underlying price is higher up the 2 center strikes, the strategy would be slightly bearish. A Short Iron Condor has two breakeven points: lower and upper. The position is profitable every bit long as the underlying price is within the two breakeven points and is unprofitable when the underlying price is outside either of the two breakeven points. Both profits and losses under this strategy are express. Maximum profit occurs when the underlying price is between the 2 center strikes, while maximum loss occurs when the underlying either falls below the lower strike or rises above the higher strike.

A Brusk Iron Condor is a net credit strategy. In terms of the gamble reward contour, a Short Iron Condor is quite attractive. In absolute terms, the maximum potential profit nether this strategy tends to be larger than the maximum potential loss. As a result, this strategy can exist initiated by intermediate option traders also. Also, equally we shall later on see, Short Iron Condor has a similar payoff construction as a Long Telephone call Condor or a Long Put Condor. Even so, there are differences. The major difference is that Long Telephone call/Put Condor are net debit strategies, while a Short Iron Condor is a net credit strategy.

Benefits of the Strategy

-

This is a net credit strategy

-

The take a chance of this strategy tends to be smaller than the potential reward

-

Time decay benefits the position, as long every bit it is profitable

-

Maximum loss under this strategy is express

Drawbacks of the Strategy

-

When the underlying price is between the middle strikes, rise in volatility would hurt the position

-

If the underlying toll moves exterior one of the two breakeven points, the trader will incur a loss

Strategy Suggestions

-

Ensure that you expect the underlying to remain in a range and consolidate near the two middle strikes

-

Ensure that yous have a bearish stance on volatility, which you expect to reduce once the position has been initiated

-

Ensure that the strikes are evenly placed. In other words, run across that the distance between the lower and the lower middle strike is equal to that between the college middle and the college strike

-

All the same, sometimes, traders keep the distance betwixt the lower heart and the higher middle strikes slightly wider than the other ii to account for a larger maximum profit zone

-

The spread between the strikes will be a trade-off between the risk and the reward

-

The wider the difference betwixt the adjacent strikes, the higher will exist the adventure but and then would exist the advantage, and vice versa

-

Too, the wider the difference between the adjacent strikes, the larger would be the profit making zone, and vice versa

-

Equally this is a range leap strategy that benefits from falling volatility, ensure that you execute this strategy when at that place is less time to expiration, every bit this would requite you lot less time to go wrong

-

Ensure at that place is sufficient liquidity in the underlying that is existence chosen to initiate this strategy

Option Greeks for Short Fe Condor

| Greek | Notes |

| Delta | Delta is at or near zero at initiation. It tends to top out higher up zippo when the underlying price is below the lower strike and bottom out beneath nada when the underlying cost is above the college strike. That said, while Delta does become not-zero every bit the underlying price moves, it does not deviate much from zero. As such, changes in the cost of the underlying do non have much affect on this strategy because of the way it is structured. |

| Gamma | Gamma is negative and is at its lowest bespeak in between the two middle strikes. As the underlying cost starts moving abroad from the midpoint of the two center strikes and approaches either the lower or the college strike, Gamma tends to move into positive earlier peaking out effectually these extreme strikes. |

| Vega | Vega is negative and is at its lowest point betwixt the 2 middle strikes, significant the negative touch of a ascent in volatility is the highest around the middle strikes. Volatility hurts equally long as the position in profitable. That said, Vega turns positive when the position becomes unprofitable, meaning a rising in volatility now starts helping the position. |

| Theta | Theta is positive and is at its highest bespeak between the two centre strikes, meaning fourth dimension disuse is most helpful around the middle strikes. Time decay benefits the position as long as information technology is assisting. That said, Theta turns negative when the position becomes unprofitable, meaning time decay now starts hurting the position. |

Payoff of Short Iron Condor

.PNG)

The higher up is the payoff nautical chart of a Short Iron Condor strategy. Detect that the strategy achieves its maximum profit potential when the underlying toll is within the range of the two heart strikes. On the other mitt, if the underlying price falls below the lower strike or rises in a higher place the college strike, the strategy achieves its maximum loss potential. Finally, notice that the strategy is profitable when the underlying price is inside the ii breakeven points and is unprofitable when the underlying price moves outside either of the two breakeven points.

Instance of Brusque Fe Condor

Let us say that Mr. ABC has decided to execute a Short Iron Condor strategy on TCS. The details of the strategy are equally below:

-

Strike price of OTM long Put = 1940

-

Strike price of OTM brusque Put = 1980

-

Strike price of OTM brusk Call = 2020

-

Strike toll of OTM long Call = 2060

-

LongPut premium (lower strike) = ₹4

-

Curt Put premium (lower middle strike) = ₹13

-

Short Call premium (higher middle strike) = ₹24

-

Long Phone call premium (higher strike) = ₹9

-

Net Credit = ₹24 (13 + 24 - 4 - nine)

-

Net Credit (in value terms) = ₹half-dozen,000 (24 * 250)

-

Lower Breakeven signal = 1956 (1980 - 24)

-

Upper Breakeven bespeak = 2044 (2020 + 24)

-

Maximum advantage = ₹6,000

-

Maximum chance = ₹four,000 ((1980 - 1940 - 24) * 250)

Now, let us presume a few scenarios in terms of where TCS would be on the expiration date and the touch this would accept on the profitability of the merchandise.

| Underlying price at Expiration | Net Profit/Loss | Notes |

| 1700 | Loss of ₹4,000 | Payoff = [Maximum of (1940-1700,0)-four]+[thirteen-Maximum of (1980-1700,0)] + [24-Maximum of (1700-2020,0)] + [Maximum of (1700-2060,0)-9]. Every bit the underlying price at expiration is below the lower breakeven bespeak, the trader will incur a loss |

| 1850 | Loss of ₹4,000 | Payoff = [Maximum of (1940-1850,0)-four]+[13-Maximum of (1980-1850,0)] + [24-Maximum of (1850-2020,0)] + [Maximum of (1850-2060,0)-ix]. As the underlying price at expiration is below the lower breakeven point, the trader will incur a loss |

| 1940 | Loss of ₹4,000 | Payoff = [Maximum of (1940-1940,0)-4]+[13-Maximum of (1980-1940,0)] + [24-Maximum of (1940-2020,0)] + [Maximum of (1940-2060,0)-ix]. As the underlying cost at expiration is below the lower breakeven point, the trader will incur a loss |

| 1950 | Loss of ₹1,500 | Payoff = [Maximum of (1940-1950,0)-4]+[xiii-Maximum of (1980-1950,0)] + [24-Maximum of (1950-2020,0)] + [Maximum of (1950-2060,0)-nine]. As the underlying toll at expiration is beneath the lower breakeven signal, the trader will incur a loss |

| 1956 | No profit, No loss | Payoff = [Maximum of (1940-1956,0)-4]+[13-Maximum of (1980-1956,0)] + [24-Maximum of (1956-2020,0)] + [Maximum of (1956-2060,0)-ix]. As the underlying price at expiration is equal to the lower breakeven point, the trader will neither brand a profit nor incur a loss |

| 1970 | Profit of ₹iii,500 | Payoff = [Maximum of (1940-1970,0)-4]+[13-Maximum of (1980-1970,0)] + [24-Maximum of (1970-2020,0)] + [Maximum of (1970-2060,0)-ix]. Equally the underlying price at expiration is between the two pause evens, the trader will make a profit |

| 1980 | Turn a profit of ₹half-dozen,000 | Payoff = [Maximum of (1940-1980,0)-4]+[13-Maximum of (1980-1980,0)] + [24-Maximum of (1980-2020,0)] + [Maximum of (1980-2060,0)-9]. As the underlying price at expiration is betwixt the two break evens, the trader volition make a turn a profit |

| 2000 | Profit of ₹half dozen,000 | Payoff = [Maximum of (1940-2000,0)-4]+[13-Maximum of (1980-2000,0)] + [24-Maximum of (2000-2020,0)] + [Maximum of (2000-2060,0)-9]. As the underlying price at expiration is between the two suspension evens, the trader will make a profit |

| 2020 | Profit of ₹6,000 | Payoff = [Maximum of (1940-2020,0)-4]+[13-Maximum of (1980-2020,0)] + [24-Maximum of (2020-2020,0)] + [Maximum of (2020-2060,0)-9]. Equally the underlying price at expiration is between the two break evens, the trader volition make a profit |

| 2030 | Profit of ₹three,500 | Payoff = [Maximum of (1940-2030,0)-iv]+[13-Maximum of (1980-2030,0)] + [24-Maximum of (2030-2020,0)] + [Maximum of (2030-2060,0)-9]. Every bit the underlying cost at expiration is betwixt the 2 suspension evens, the trader will make a profit |

| 2044 | No profit, No loss | Payoff = [Maximum of (1940-2044,0)-4]+[13-Maximum of (1980-2044,0)] + [24-Maximum of (2044-2020,0)] + [Maximum of (2044-2060,0)-9]. Every bit the underlying price at expiration is equal to the upper breakeven signal, the trader volition neither make a profit nor incur a loss |

| 2050 | Loss of ₹1,500 | Payoff = [Maximum of (1940-2050,0)-4]+[xiii-Maximum of (1980-2050,0)] + [24-Maximum of (2050-2020,0)] + [Maximum of (2050-2060,0)-9]. As the underlying price at expiration is above the upper breakeven point, the trader will incur a loss |

| 2060 | Loss of ₹4,000 | Payoff = [Maximum of (1940-2060,0)-4]+[13-Maximum of (1980-2060,0)] + [24-Maximum of (2060-2020,0)] + [Maximum of (2060-2060,0)-9]. As the underlying price at expiration is in a higher place the upper breakeven point, the trader will incur a loss |

| 2150 | Loss of ₹4,000 | Payoff = [Maximum of (1940-2150,0)-4]+[13-Maximum of (1980-2150,0)] + [24-Maximum of (2150-2020,0)] + [Maximum of (2150-2060,0)-9]. As the underlying cost at expiration is in a higher place the upper breakeven bespeak, the trader will incur a loss |

| 2300 | Loss of ₹four,000 | Payoff = [Maximum of (1940-2300,0)-4]+[xiii-Maximum of (1980-2300,0)] + [24-Maximum of (2300-2020,0)] + [Maximum of (2300-2060,0)-9]. Every bit the underlying cost at expiration is to a higher place the upper breakeven point, the trader will incur a loss |

Notice to a higher place that maximum turn a profit for this strategy is ₹6,000, which the trader earns when the underlying price stays inside the two middle strikes of 1980 and 2020. On the other hand, notice that maximum loss for this strategy is ₹4,000, which occurs when the underlying price either falls below the lower strike of 1940 or rises higher up the higher strike of 2060. Also detect that with a maximum possible profit of ₹6,000 and a maximum possible loss of ₹four,000, the risk advantage for this strategy stands at ane.5 .

Next Chapter

Responses

Source: https://fyers.in/school-of-stocks/chapter/options-strategies/long-iron-condor-and-short-iron-condor.html

Posted by: garciaestre1969.blogspot.com

0 Response to "How To Repair A Broken Iron Condor"

Post a Comment